Following our Creative Economies Reports, we publish regularly updates of the ZCCE Creative Industries Economic Measures Switzerland.

This statistical analysis approaches the creative economies from an industry-based perspective along various submarkets.[1] It presents information on the creative enterprises – that is businesses and employees active in the creative industries sector – and their contribution to Swiss economic activity.

Mapping the Creative Industries Switzerland

Our research allows us to analyse the size, importance, trends and regional geography of the creative industries and its 13 submarkets in Switzerland.

Looking at the data, we can explore the number of businesses, employees, full time equivalents, generated gross value added and turnover of the creative industries and its 13 submarkets as well as the development over time and the local importance and specialisation in the cantons.

Source: FSO, STATENT, NA; STATZH, DISAGG-GVA; FTA, VAT; own calculations by Zurich Centre for Creative Economies (ZCCE) at ZHdK

Overview

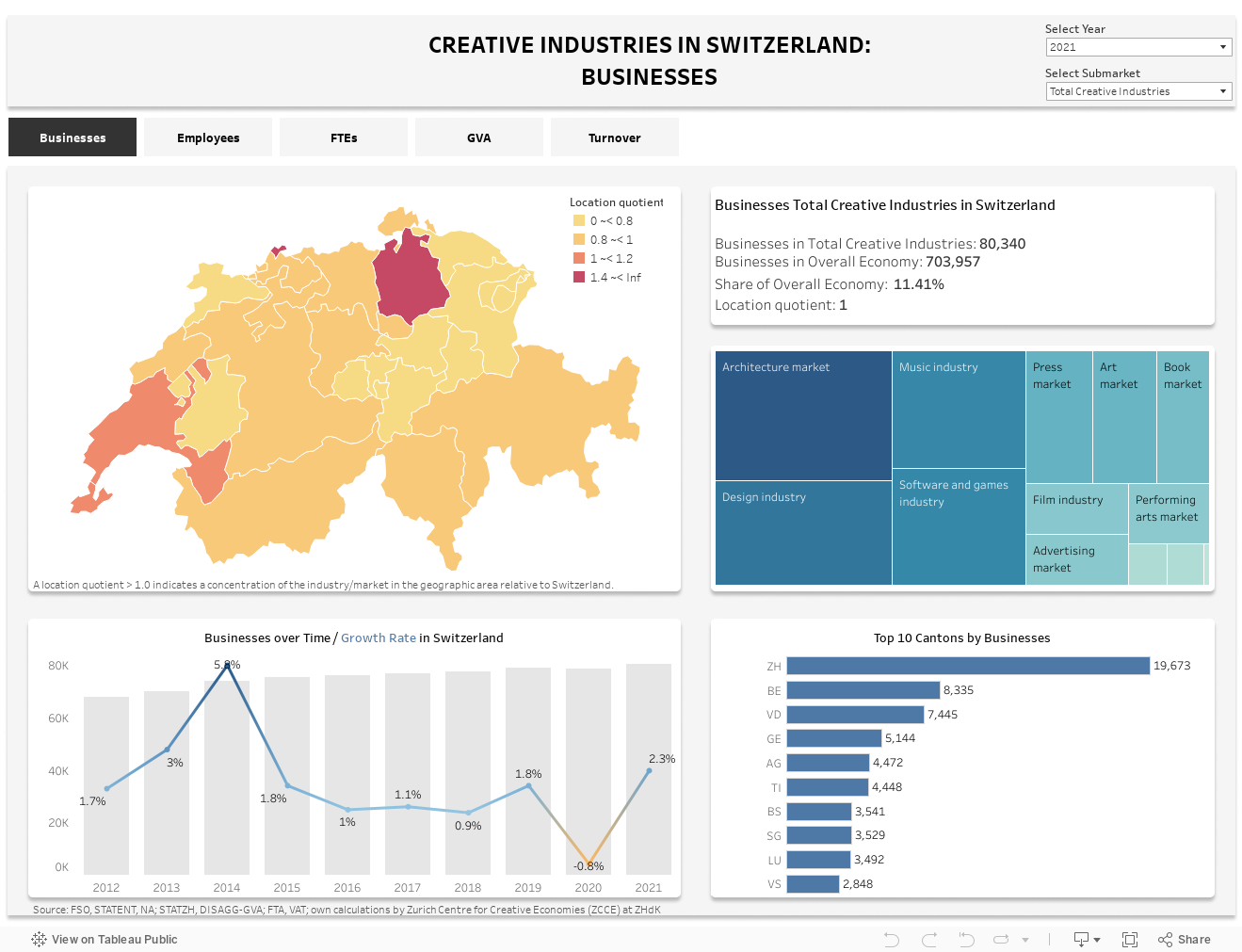

In 2021, around 303,000 persons were employed in Switzerland’s creative industries in roughly 80,000 businesses. This represented 11.4% of Swiss businesses and 5.6% of all employees. The creative industries generated an estimated Gross Value Added (GVA) of CHF 27 billion and an estimated turnover of CHF 99 billion. This corresponded to almost 3.8% of Switzerland’s GVA and 2.1% of Switzerland’s total turnover.

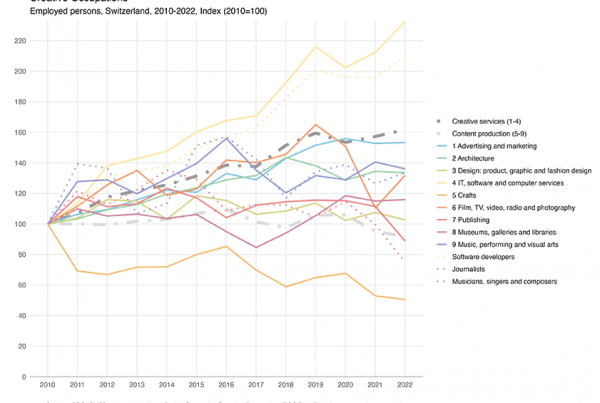

Employment in Switzerland’s creative industries is highest in the submarkets Software and games industry (68,309, 22.6% of creative industries), Architecture market (59,728, 19.7%), Music market (31,044, 10.3%), Design industry (26,756, 8.8%) and Press market (23,584, 7.8%). These five submarkets account for more than two thirds of all creative industries jobs.

The figures confirm that the Switzerland’s creative industries are dominated by small businesses. 93% are micro-businesses employing up to 10 persons (FTEs). Around three quarters (78%) comprise merely one or two persons. Such businesses are known as smallest, i.e., micro-businesses. The pie chart shows that more than two fifth (43.6%) of all Switzerland’s creative industries employees work in micro-businesses, i.e., in businesses with less than 10 employees.

The creative industries are particularly concentrated (LQ > 1.2) in the canton ZH (% of total employment = 8.2%, LQ = 1.5), ZG (7.5%, 1.3) and BS (7.0 %, 1.3).

Developments

The Covid-19 pandemic has had a major impact on the creative industries. In the first year of the pandemic in 2020, the number of creative businesses fell by 0.8% compared to the previous year (compared to -0.2% for the overall economy), having previously increased continuously since 2011.

In 2021, the creative sector recorded 1,840 more businesses than in 2020, with a total of 80,340 creative businesses. This figure is higher than before the Covid-19 pandemic and represents a new high since 2011. The increase in the creative industries (+2.3%) was therefore higher than in the overall economy (+1.3%). It was most pronounced in Film industry (+6.9%), Software and games industry (+4.1%) and Design industry (+3.9%).

The number of employees in the creative industries, which also had increased constantly since 2011, rose by 10,146 employees (+3.5%) to 302,627 employees, which is also more sharply than in the overall economy (+2.4%). The increase was highest in Software and games industry (+6.5%), Film industry (+5.8%) and Music industry (+4.8%).

The effects of the pandemic are also still visible in the macroeconomic indicators of the creative industries. With the outbreak of Covid-19, the creative sector’s nominal gross value added shrank by 3.4% in 2020 compared to 2019 (overall economy -2.8%).

In 2021, nominal gross value added in the creative industries climbed back at CHF 27.4 billion. At +5.2%, the increase in nominal gross value added in the creative sector between 2020 and 2021 was lower than that in the overall economy (+6.6%).

Among the strongest increase in nominal gross value added in the creative industries sector in 2021 was in Performing arts market (+13.3%) and Music industry (+7.4%), where it had recorded the sharpest decline in 2020 (-50.0% resp. -33.9%).[2] That year, many cultural institutions had to close temporarily due to the pandemic.

Methodology

Based on the classification for creative industries according to ZCCE, we calculate the size and the development of the creative industries and its 13 submarkets in Switzerland using the Structural Business Statistics (STATENT), the National Accounts (NA) and the Value Added Tax (VAT).[3]

In Switzerland, the creative industries sector is defined, with reference to the European debate, as those cultural and creative enterprises that are predominantly market oriented and are concerned with the production, distribution and media dissemination of cultural and creative goods and services.

The creative industries Switzerland are subdivided into 13 submarkets.[4] It is here that products and services are created, either for other production and service sectors or directly for the final consumer market. In this sense, the cultural and creative industries are mainly assigned to the private sector of cultural production – thus neither to the public sector (public cultural promotion) nor to the intermediate sector (foundations, associations). However, artists and creative professionals are often active in all three sectors. From their point of view, the three submarkets should be seen as parts of the same system. In addition to its own market structures, the cultural and creative industries also build on the creative potential of the public and non-profit sub-sectors and has an innovative effect on them. Therefore, the cultural and creative industries can only be seen as a holistic system.[5]

Further information in our Creative Economies Reports and in the Research Notes.

Notes

[1] See also our complementary analysis on creative workers, that is the employed persons working in the creative sector as well as persons working in creative occupations outside the creative industries.

[2] The real development of GVA is not (yet) available for methodological reasons. However, the structural business statistics (STATENT) only partially reflects the pandemic’s impact: Thanks to short-time working and loss of earnings allowances, a significant proportion of Old-age and survivor’s insurance (OASI) contributions continued to be paid, even when employees were prohibited from carrying out their work. The data underlying STATENT cannot therefore fully reflect the declines in activity in some sectors. A specific series for the years affected by COVID-19 must therefore be constructed (see FSO, experimental statistics).

[3] See Christoph Weckerle, Simon Grand, Frédéric Martel, Roman Page and Fabienne Schmuki, Entrepreneurial Strategies for a Positive Economy, 3rd Creative Economies Report Switzerland, Zürich 2018.

See Christoph Weckerle, Roman Page, Simon Grand: Von der Kreativwirtschaft zu den Creative Economies. Kreativwirtschaftsbericht Schweiz, Zürich 2016.

[4] See the classification of creative industries according to the approach used by the ZCCE in the annexe.

[5] See Christoph Weckerle, Hubert Theler, Die Bedeutung der Kultur- und Kreativwirtschaft für den Standort Zürich, Dritter Kreativwirtschaftsbericht Zürich, ZHdK 2010.